Proposed autónomo tariffs in Spain 2026-2028 - comparison and response

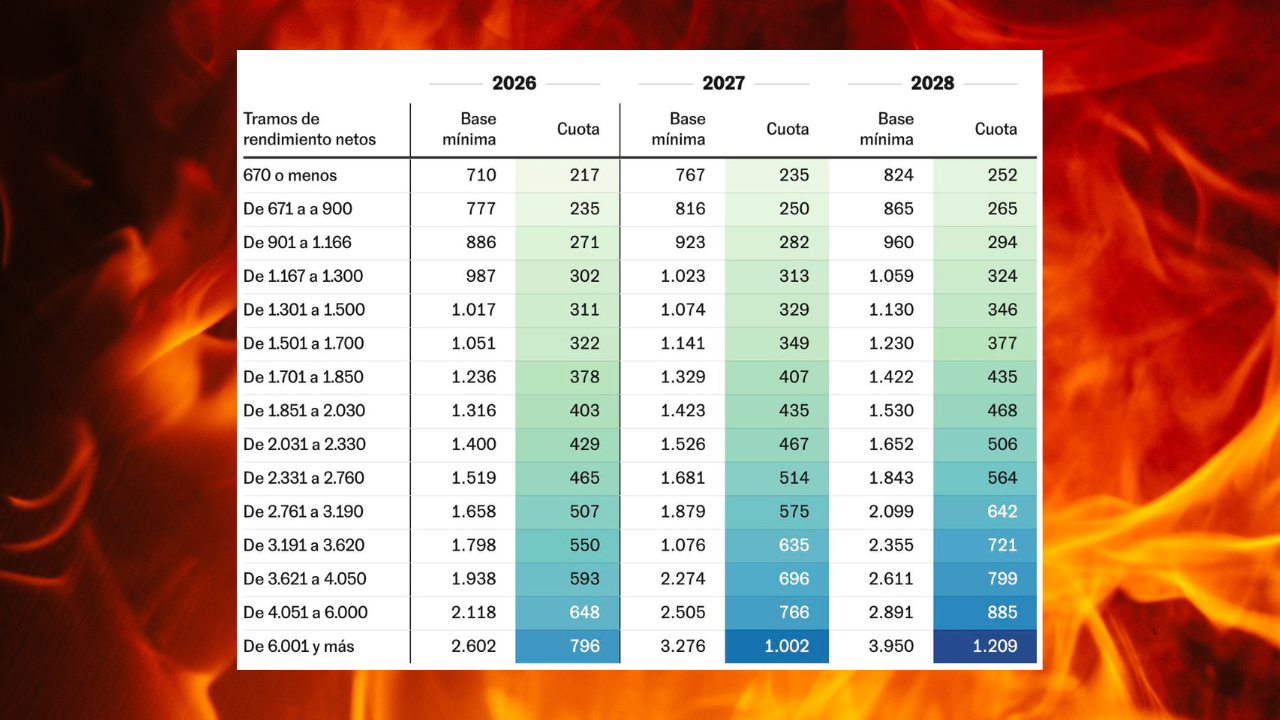

In October 2025, Spain’s Ministry of Inclusión, Seguridad Social y Migraciones officially published a new proposal for freelancer (“autónomo”) social security quotas, outlining base monthly contributions and payment bands for 2026, 2027, and 2028. The data, which is circulating widely on social media, comes directly from tables presented by the government in meetings with worker associations and unions. It specifies 15 income tranches with distinct social security payments, progressively increasing over time.

The figures you see (like €217 minimum monthly payment for the lowest earners in 2026, rising to €796 for those earning €6,000+) are drawn from the official documentation delivered to entities such as ATA (Asociación de Trabajadores Autónomos), UPTA, and UATAE, as well as employers’ groups, and published in major Spanish news outlets and government portals.

How was the data published and by whom?

The recent proposal was presented by Spain’s Ministry of Inclusión, Seguridad Social y Migraciones during a series of meetings in October 2025. These proposals are then reviewed at the Mesa de Diálogo Social, where government officials, unions, and business associations debate the details and future structure of freelancer contributions. Media coverage and official statements confirm direct government involvement, with documentation released both formally and informally to sector representatives.

What does it mean? Who must approve it?

The proposed quotas are not yet final law—they require approval through Spain’s parliamentary process. First, consensus is sought at the Mesa de Diálogo Social: unions, employer organisations, and freelancer associations discuss potential impacts and propose amendments. Once basic agreement is reached, the government drafts a formal decree law, which must then be validated by the Spanish Parliament (Congreso de los Diputados). A majority vote is needed for approval.

If significant disagreement remains, the proposals may be subject to further parliamentary negotiation and amendment, potentially leading to delays or modifications. After parliamentary ratification, publication in the Boletín Oficial del Estado (BOE) formalises the rates and triggers their legal implementation.

Who is considering the data, and who’s opposed?

Stakeholders include the major freelancer associations (ATA, UPTA, UATAE), trade unions, employer organisations, and government ministries. Some groups, notably ATA - the only body truly independent from the government - have expressed strong opposition, citing concerns over the increased financial burden on small businesses and self-employed workers.

On the other hand, union groups generally advocate for more progressive contributions tied to actual income, seeking enhanced transparency and social protection for freelancers.

When will we know more?

Negotiations are ongoing, with another round of deliberations expected before the end of 2025. The Spanish government has set a target for finalising the quota structure by late December 2025, aiming for implementation beginning 1 January 2026. If parliamentary debate leads to substantial amendments or delays, the process could be extended into early 2026 before final figures are confirmed.

What does this mean in the European context?

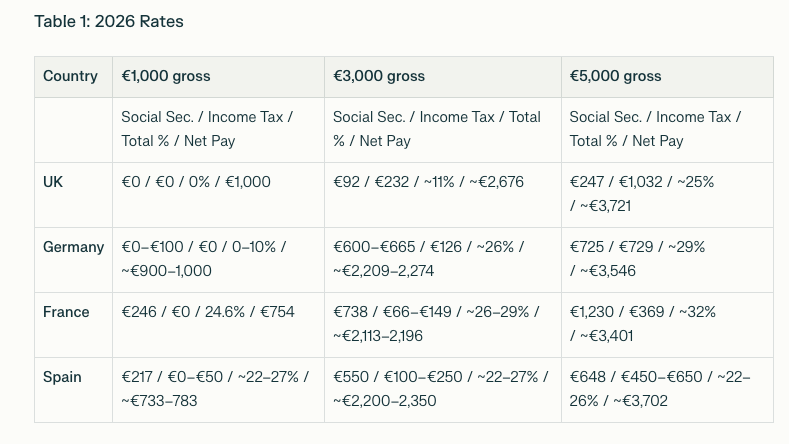

To understand the impact, we looked at comparable total tax take (social security + income tax) for freelancers, across 4 different markets, and 3 different levels of earnings:

Reviewing the 2026 and 2028 rates tables reveals clear disparities in the tax and social security burden borne by freelancers across countries and income bands*.

For low earners under €1,000, the UK imposes virtually no combined taxes, offering near-full net take-home pay, while Germany and France place notable social charge burdens, with France’s flat-rate social charges disproportionately impacting smaller incomes. Spain’s new proposed quotas for 2026 and 2028 appear comparable to France, creating a significant fixed minimum load on low earners.

At the €3,000/month level, Germany exhibits the highest combined tax/social charges, largely driven by mandatory health insurance contributions, followed closely by France and Spain, both showing 25–33% effective rates. By €5,000/month, the tax bite deepens substantially across all markets, but France’s progressive income tax and social contributions push its freelancers to the highest effective rates near 36% by 2028. Meanwhile, the UK remains the most favourable location overall, with moderate rates even at higher income levels.

This analysis underscores that freelancers in Germany and France (and increasingly Spain) face the steepest effective contributions, particularly as income rises beyond basic subsistence, while the UK system maintains the lightest burden.

Furthermore, there is data indicating that typical freelancers in Spain frequently encounter lower hourly pay rates than their counterparts in the UK, Germany, and France, which is compounded by their comparatively high social security costs to reduce net income. This aligns with cost of living and market maturity factors often cited in Europe-wide freelance income analyses. It’s easy to say that freelancers should simply raise their rates, to support a highre tax take - however in competitive markets like language tutoring or basic tech roles, there’s very little scope to negotiate with clients without simply pricing out of the market altogether.

Remote Work Europe’s response:

In the context of ongoing budgetary deficits and public finance pressures across the UK, Germany, France, and Spain, we understand that these rising social security contributions and tax burdens on freelancers reflect broader fiscal challenges. Eurozone countries, including France, Germany, and Spain, continue navigating deficits above the EU’s reference level of 3% of GDP, with Spain gradually reducing its deficit but still facing structural expenditure demands. Governments are under pressure to stabilize public finances while funding social protections and investment priorities.

However, the sharp impact on low-earning freelancers, particularly in Spain where fixed social security charges form a large proportion of modest incomes, raises big questions of fairness and economic sustainability. Many freelancers already operate near subsistence levels; imposing high proportional payments risks pushing vulnerable entrepreneurs into financial hardship. Balancing fiscal responsibility with equitable treatment of the self-employed remains a critical policy challenge. Ideally, reforms would ensure progressive contributions aligned with true ability to pay, mitigating burdens on low earners while securing social protections and public revenues for the long term.

Instead we contend that these changes, if implemented, will drive many freelancers in Spain in particular out of the market altogether - lower earners will not find it sustainable to remain self-employed, and as this is being implemented in conjunction with greater digital transparency in invoicing, others will resort to greater use of cash and alternative means of exchange of value, further reducing treasury receipts.

Higher earning freelancers meanwhile are also those most likely to be highly personally mobile, and able to choose where they want to live and be tax resident. Many of these are also likely to be the most creative and innovative entrepreneurs in the country, the very people the essential to growth and job creation in local economies.

(Social security contributions reach their capped quota maximum starting at the €6,000 income bracket, so the social payment is flat at about €796 in 2026 and rises to €1,209 in 2028. Income tax rises significantly with income, explaining the increase in total effective tax and net take-home pay reduction.)

So why on earth would such entrepreneurs choose to relocate to - or stay - in Spain, if it’s going to cost them 38% of their gross income within a few years’ time?

*Notes on calculations/assumptions:

UK: 20% income tax above personal allowance, 40% above £50,270 (€58,000 in 2025), Class 4 NICs at 6–2%.

Germany: Health insurance scales from €600–810/month as income rises; includes progressive federal tax and basic allowances.

France: Auto/micro-entrepreneur capped at thresholds; standard social contributions and progressive tax used for high incomes.

Spain: Social security cuota for €5k/month earnings is €648 in 2026, €885 in 2028; income tax estimated on taxable base assuming standard deductions.

Net take-home is always gross – (social security + income tax).